The delayed energy transition – Wood Mackenzie

The world is heading for a 3°C warming trajectory. Energy transition is delayed due to political headwinds

WoodMac’s report examines the impact of a delayed energy transition amid political uncertainty, inflation and elections around the world.

London, May 2, 2024 – If the energy transition is delayed by five years, global average temperatures could rise by 3°C above pre-industrial levels, according to Wood Mackenzie’s latest analysis, Delaying the Energy Transition. .

Wood Mackenzie’s Energy Transition Delay Scenario analyzes the impact of a five-year delay on global decarbonization efforts and projects average annual spending to fall to US$1.7 trillion. This is 55% lower than Wood Mackenzie’s 2050 Net Zero Scenario*, which mapped out what it would take to meet the goals of the Paris Agreement.

In terms of total investment, the costs of a delayed transition could reach up to $48 trillion, a significant reduction from Wood Mackenzie’s net-zero scenario, which estimates a total of $75 trillion. Capital spending in the oil and gas sector is expected to rise to 31%, while spending in the power sector is expected to remain at the current level of 60%, with a delayed transition. If the power sector captures 80% of total spending, spending could fall to less than 10% in a net-zero scenario.

For the metals and mining sector, capital investment is the most resilient, remaining at around 6% of the total across all scenarios. In contrast, despite their critical role in the overall energy transition, hydrogen and carbon investment, capture, utilization and storage (CCUS) remains at 8% compared to Wood Mackenzie’s net-zero scenario. and decreases to 2%.

“As half of the world’s population heads to the polls in 2024, political realities and skepticism about climate change in major emitters such as the United States and Europe are driving the issue as voters seek economic security and price stability,” Prakash said. Support for the transition may decline.” said Sharma, vice president of scenarios and technology at Wood Mackenzie and author of the report.

“The global stocktake at COP28 in December 2023 shows that major countries are still not on track to achieve the Paris agreement, and that strong policy measures and capital investment are needed to accelerate the transition. Indeed, Europe and the UK have already pushed back their 2030 climate targets, and other countries may follow suit,” Sharma added.

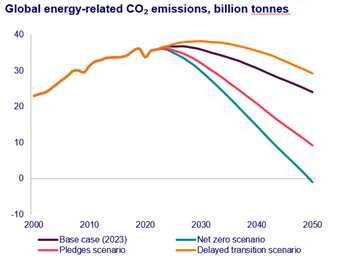

According to this scenario, emissions are expected to peak in 2032, and the remainder of the global carbon budget at a temperature of 1.5°C will be exhausted by 2027, meeting the Paris Agreement targets by 2050. The ability of countries to achieve this will further weaken.

In Wood Mackenzie’s delayed scenario, renewable energy-led electrification is likely to become increasingly difficult. In the long term, solar and wind power will dominate the electricity market, but transmission bottlenecks are slowing short-term additions to the electricity market. Unabated heat supply enables flexible power generation to balance the power grid.

Rising interest rates and supply chain bottlenecks have increased the cost of renewable energy by 10% to 20% in recent years. The high cost of renewable energy will further slow the decline in the cost of low-carbon hydrogen, with demand expected to fall to 100 million tonnes (Mt) in 2050, nearly 50% less than in the base case.

Delaying the transition means carbon capture and removal technologies will need to play a key role in restoring carbon balance and achieving long-term climate goals. With Wood Mackenzie’s delayed transition, CCUS intake is expected to reach 225 million tonnes by 2030 and continue to grow as policy incentives expand and storage infrastructure is built.

In the late-transition scenario, oil demand would peak at 114 million barrels per day (mb/d) in 2033, 6 mb/d lower than in the base case due to slower adoption of electric vehicles (EVs) outside China. Will increase soon. Gas demand will peak at 4,536 billion cubic meters (bcm) of natural gas in 2045, an increase of nearly 100 bcm over the reference case. Meanwhile, coal demand has declined modestly and remains on a trajectory 3% higher than the base case for this decade.

“Renewables and reduced hydrogen production provide headroom for further gas demand growth, but coal resilience limits upside. Commodity markets will tighten further unless investment in supply increases. , the instability is likely to be prolonged,” Sharma said.

end

Editor’s note:

This report is part of Wood Mackenzie’s Energy Transition Outlook series.

Wood Mackenzie released its latest base scenario outlook in September 2023. Since then, policy and political changes, particularly in some major economies, have increased the risk of delaying the transition to low-carbon energy. As a result, we publish here an energy transition delay scenario that considers the impact of his five-year delay on global decarbonization efforts.

Scenario definition*:

-

Normative example – Wood Mackenzie’s base case view across all products and technology business lines – our core and most likely outcomes.

-

Pledge scenarios of each country – Wood Mackenzie’s scenarios for how national commitments will be implemented in the future. The 2°C trajectory is consistent with the Paris Agreement temperature limit.

-

Net zero 2050 scenario – Wood Mackenzie’s scenario for how a 1.5°C world will develop over the next 30 years. Carbon emissions are in line with the most ambitious goals of the 2015 Paris Agreement.

-

Energy transition delay scenario – Impact of a 5-year lag on global decarbonization efforts modeled in the base case.

Related news and commentary

For more information, please contact us below.

Vivien Lebbon, T: +44 330 174 7486, E: Vivien.lebbon@woodmac.com

About Wood Mackenzie

Wood Mackenzie is a business that provides global insights into renewable energy, energy and natural resources. Driven by data. Empowered by people. Businesses and governments in the midst of an energy revolution need reliable and actionable insights to guide the transition to a sustainable future. That’s why, backed by over 50 years of natural resources experience, we cover the entire supply chain with unparalleled breadth and depth. Today, our team of more than 2,000 experts operates in 30 locations around the world, driving customer decisions through real-time analytics, consulting, events, and thought leadership. Together, we provide the insights you need to differentiate between risks and opportunities and make bold decisions when it matters most. For more information, please visit: woodmac.com.

attachment