’s Future Dividend")

Some investors rely on dividends to grow their wealth. If you’re also a dividend expert, you might want to know: Barrett Business Service Co., Ltd. (NASDAQ:BBSI) goes ex-dividend in four days. The ex-dividend date is his one business day before the record date and is the cut-off date on which a shareholder can be on the company’s books and receive dividend payments. When buying or selling stocks, the ex-dividend date is important because it takes at least two business days for the trade to settle. Therefore, if you purchased Barrett Business Services stock after May 16th, you will not be eligible to receive the dividend payable on May 31st.

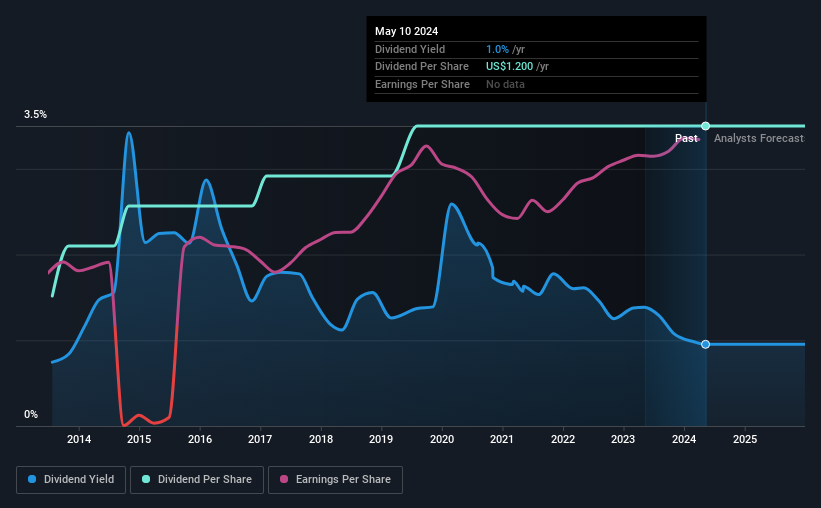

The company’s next dividend will be US$0.30 per share. Last year, the company distributed a total of $1.20 to shareholders. Calculating the last year’s worth of payments shows that Valet Business Services has a yield of 1.0% on the current stock price of $125.98. Dividends can be a significant contributor to investment returns for long-term holders, but only if they continue to be paid. So we need to investigate whether Valet Business Services can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Barrett Business Services.

Dividends are usually paid out of a company’s profits. If a company pays more in dividends than it earned in profit, then the dividend might become unsustainable. Valet Business Services pays out just 16% of its after-tax profit, which is low enough to leave plenty of headroom in the event of an adverse event. A useful secondary check is to assess whether Valet Business Services generated enough free cash flow to pay its dividend. The good news is that the company paid out just 8.8% of its free cash flow last year.

It’s reassuring to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don’t drop precipitously.

Click here to see the company’s payout ratio and analyst estimates of its future dividends.

Are profits and dividends growing?

Companies with promising growth potential are usually the ones that pay the most dividends, since it’s easier to grow dividends when earnings per share are improving. If profits decline and the company is forced to cut its dividend, investors could see the value of their investments explode. With that in mind, we’re encouraged by Valet Business Services’ steady growth, which has seen its earnings per share increase by an average of 7.9% over the past five years. Earnings per share have been steadily increasing, and management reinvests nearly all profits back into the business. If profits are reinvested effectively, this could be a bullish combination for future earnings and dividends.

The main way most investors assess a company’s dividend prospects is by looking at its historical dividend growth rate. Since our data began 10 years ago, Valet Business Services has raised its dividend by an average of about 8.7% per year. It’s encouraging to see the company raising its dividend amid growing profits, suggesting that the company has at least some interest in rewarding shareholders.

conclusion

Should investors buy Barrett Business Services for its upcoming dividend? Earnings per share growth is modest, with Barrett Business Services paying out less than half of its profits and cash flow as dividends. This is interesting for a number of reasons, as it suggests management may be reinvesting heavily in the business, while also giving it scope to increase the dividend. While it might be great to see earnings grow faster, Bullet Business Services has been conservative with its dividend payments and could still maintain reasonable performance over the long term. There’s a lot to like about Barrett Business Services, so we’ll make it a priority to take a closer look.

Curious about what the future holds for Barrett Business Services? See what the 4 analysts we track are predicting by visualizing past and future expected earnings and cash flow.

A common investment mistake is buying the first interesting stock you see.can be found here Complete list of high dividend stocks.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.